OAuth Scopes and Permissions for Embedded Accounting Platforms

How to design least-privilege access for invoices, expenses, reports, journals, and connected apps in multi-tenant accounting systems.

Evaluating this for a platform, firm, or fintech product? Explore our embedded accounting infrastructure overview

OAuth is only part of the trust model.

For embedded accounting platforms, the harder and more important question is usually:

What should an app actually be allowed to do?

That is where OAuth scopes and permissions matter.

This guide reflects how Paprel currently approaches OAuth consent, access control, and activity visibility in App Connect workflows as of June 5, 2026 and is reviewed by the Paprel Product Team.

If scope design is too broad, teams create unnecessary risk. If it is too narrow or too inconsistent, integrations become frustrating to adopt.

The goal is not to create the longest possible permissions list. The goal is to create an access model that matches real finance workflows.

Why OAuth Alone Is Not Enough

It is easy to say a platform supports OAuth and still leave the real risk unresolved.

OAuth answers part of the problem:

- who is authorizing the app

- which tenant or company is involved

- how an app gets access without receiving a raw shared credential

But OAuth by itself does not tell a user:

- which records the app can read

- whether it can create or update records

- whether it can post financial actions directly

- whether some actions stay draft-only

For finance systems, those details matter more than the protocol label.

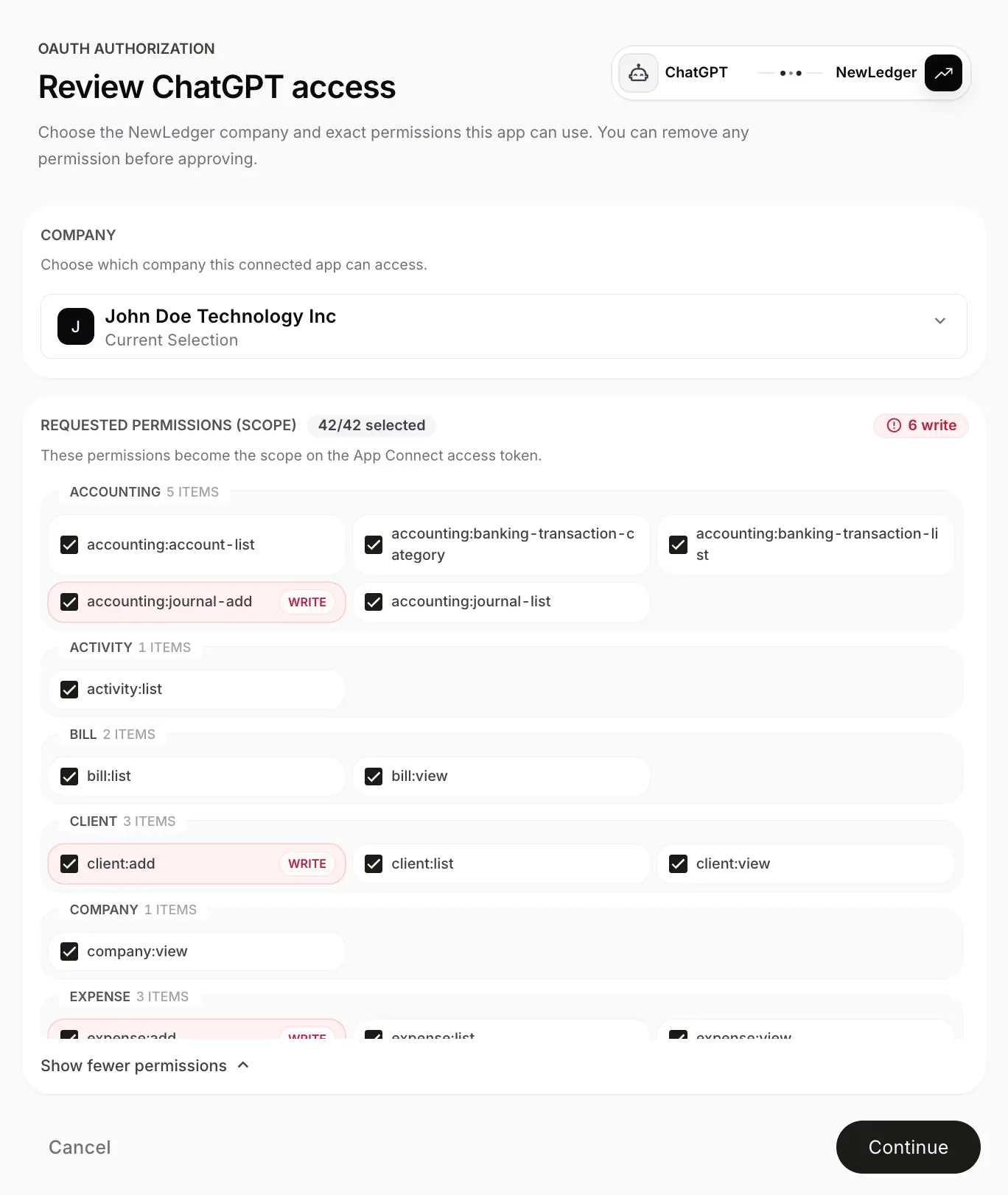

Consent should be explicit, but good consent also depends on a permission model that people can understand and trust.

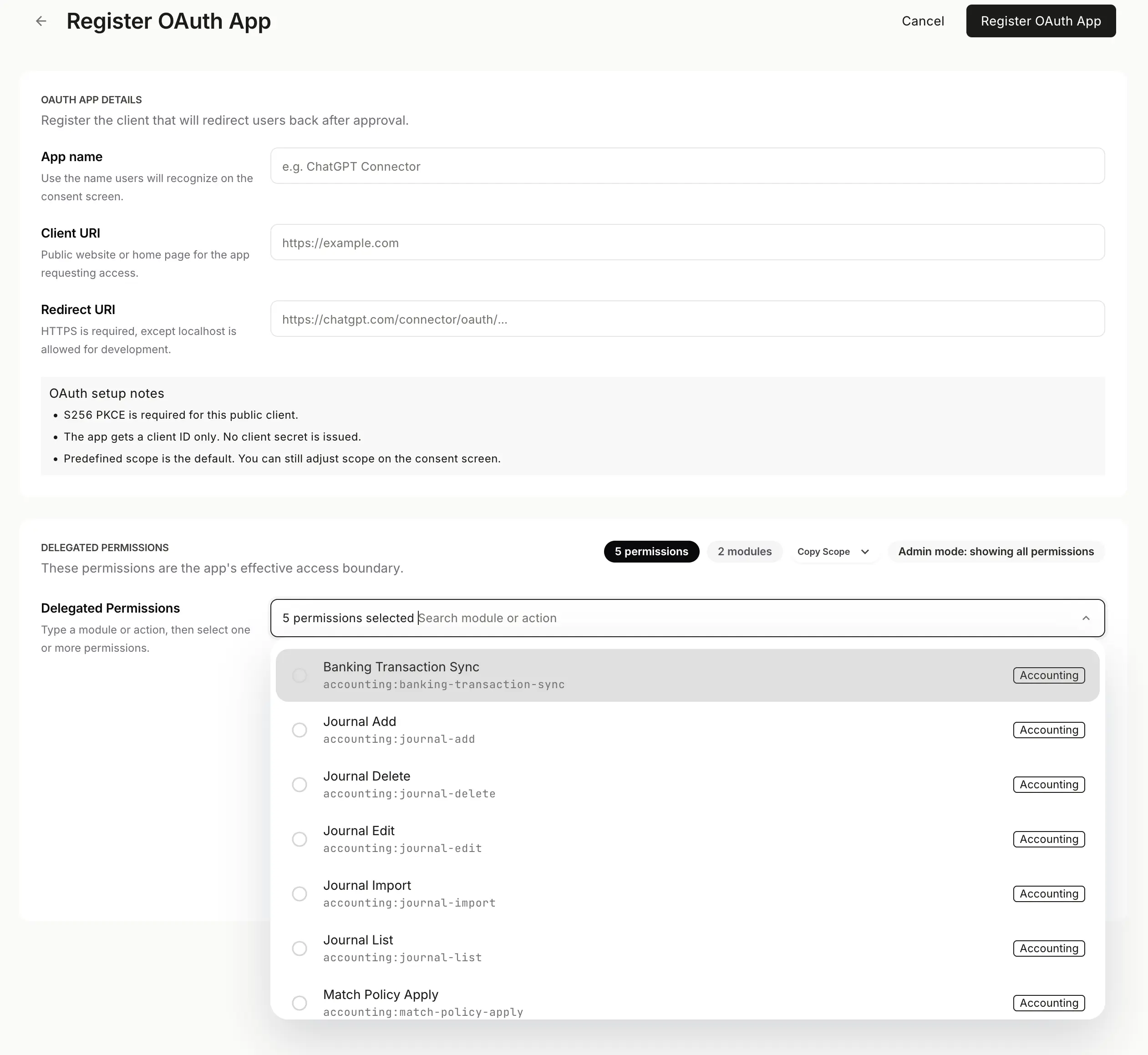

What Finance-Grade Scopes Should Protect

In embedded accounting, apps may interact with:

- invoices and customer records

- bills and vendors

- expenses and attachments

- journals and ledger activity

- reports and balances

- bank-related workflows

Those are not all the same level of sensitivity.

A useful scope model should distinguish between:

- operational context retrieval

- document preparation

- workflow updates

- accounting-impacting actions

- administrative configuration

That separation is what helps keep least-privilege access practical instead of theoretical.

Scopes Matter Beyond OAuth Too

Even when a platform supports API credentials for direct machine-to-machine access, permission design still matters.

That is because a credential can still be too broad if the platform does not define:

- what the credential is allowed to access

- which operational or finance actions it can perform

- whether it is intended for internal service access or a narrower integration path

OAuth is often the right model for delegated app installs, but scope discipline should exist in both models.

A credentials list is also part of the permissions story. Direct machine access still needs explicit boundaries and clear intent.

A strong detail view helps teams reason about scope not only during app installs, but also during direct credential provisioning and review.

Why Read And Write Are Not Enough

Many systems start with a simple permission split:

- read

- write

That is often not enough for embedded accounting.

Finance workflows usually benefit from a more structured model such as:

- read-only access for context and reporting

- create-draft access for invoices, expenses, or other documents

- review or approval-related actions

- post or finalize actions reserved for narrower roles

This matters because the difference between creating a draft expense and posting an accounting outcome is operationally significant.

An OAuth app overview should make the access model legible before a user ever reaches the consent step.

Draft-Only Actions Are A Strong Middle Ground

Some of the safest and most useful finance integrations do not need unrestricted write access.

A draft-first pattern makes it possible for an app to help with real work while preserving review boundaries.

That approach is often a better fit for:

- AI-assisted workflows

- third-party operational apps

- partner automations

- early platform ecosystems

The question is not only whether an app can write. It is whether it should be allowed to complete the full accounting consequence without review.

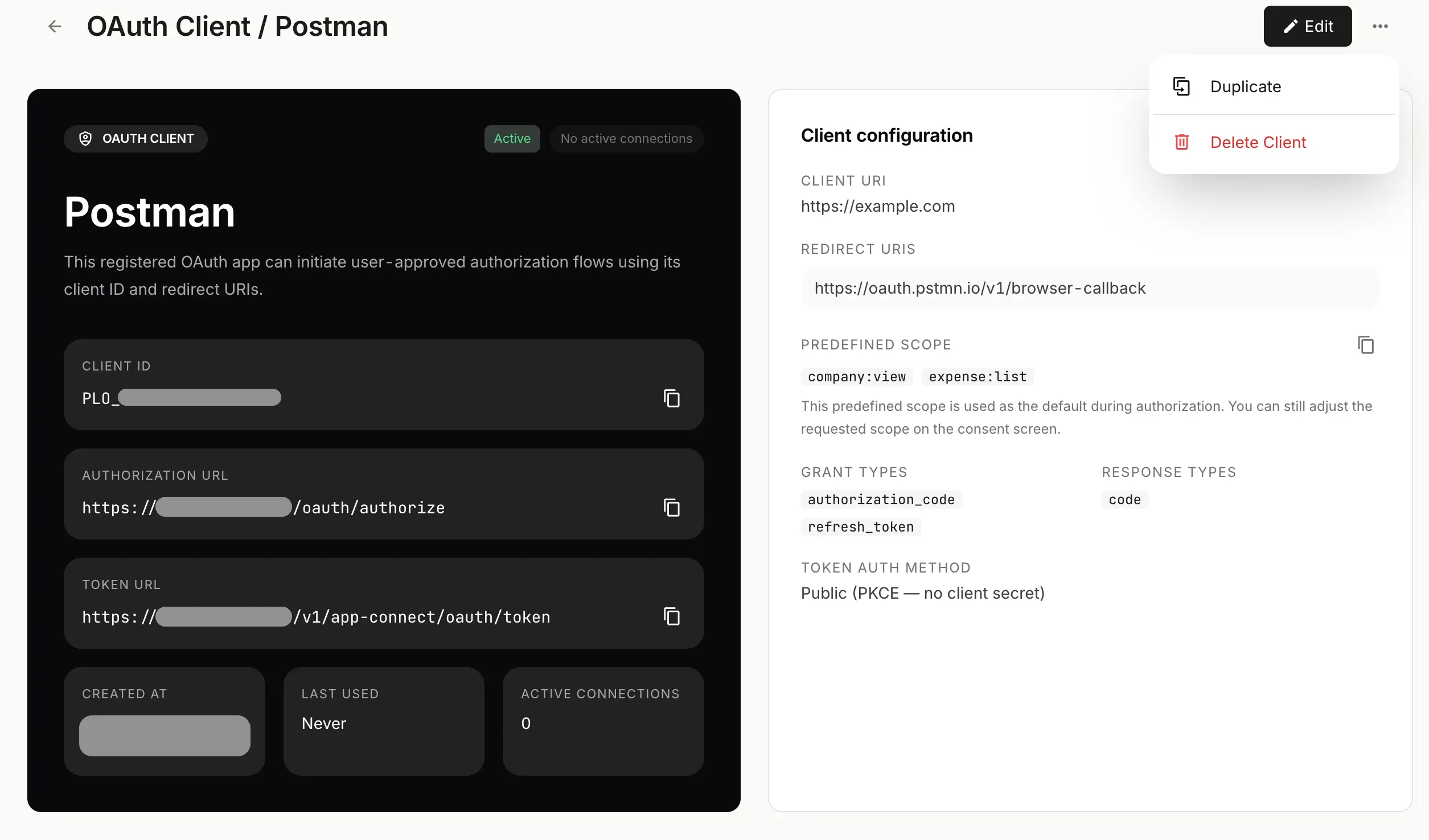

Why Tenant Boundaries Matter

Once a platform supports multiple companies or workspaces, scope design becomes inseparable from tenant design.

Teams should be able to answer:

- which company granted the permission

- whether the app can act outside that tenant

- whether permissions differ by installation

- how access is revoked for one connected app without affecting another

Without those boundaries, even a clean-looking OAuth flow can hide too much risk.

Tenant-aware detail matters because a permission boundary is only trustworthy when it stays attached to a known app and company context.

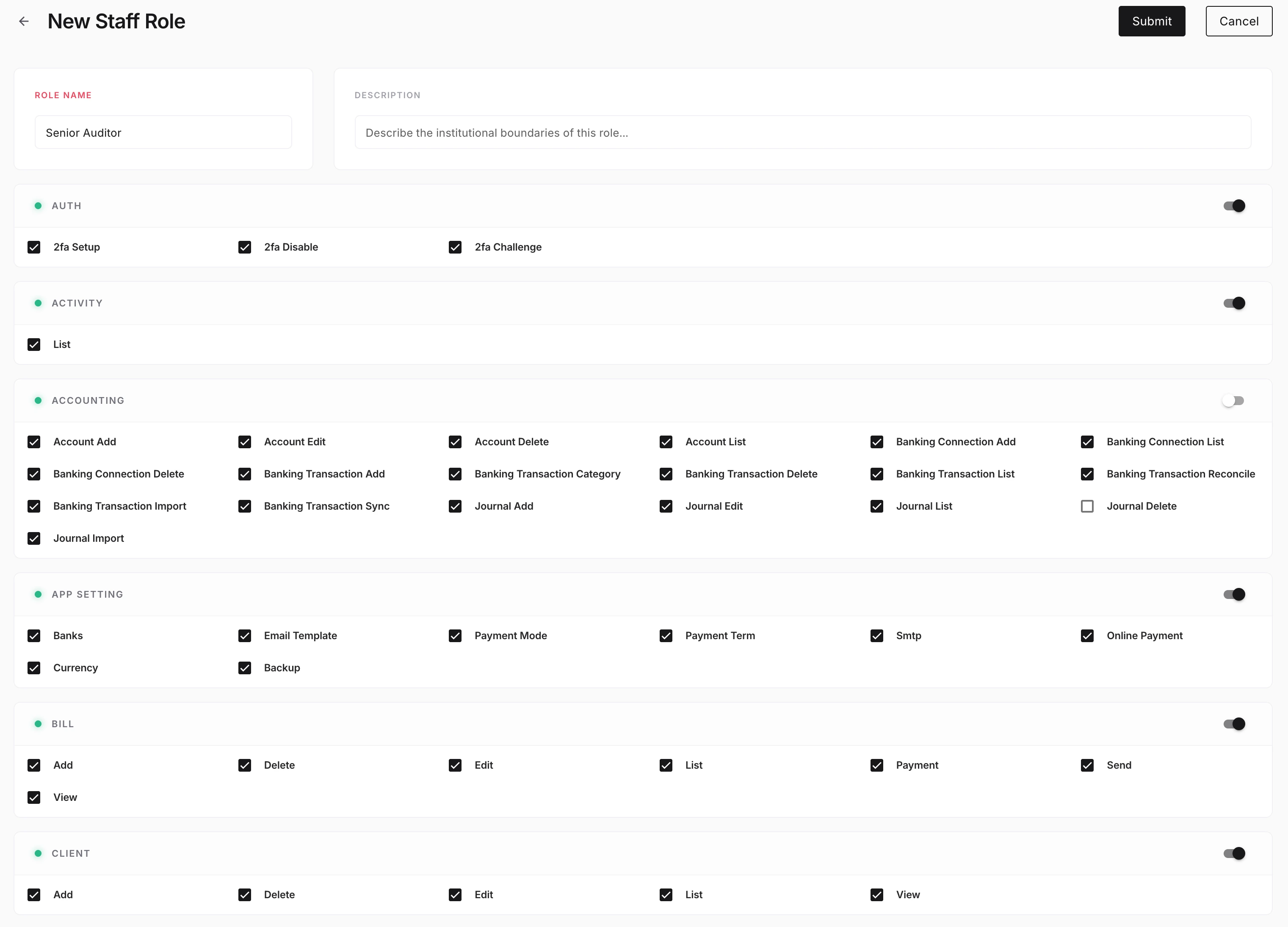

Permissions Should Reflect Real Workflow Roles

A strong permissions model usually maps to workflow reality, not to abstract API categories alone.

For example:

- an app may need access to create draft invoices but not view all journals

- a reporting integration may need read access to financial reports but no document creation rights

- an expense workflow tool may need expense-related scopes without broad admin configuration access

This is where access control design becomes product design.

Permissions become more credible when they are structured around real workflow boundaries instead of one broad access bucket.

Registration is part of the control model too. The app-install surface should reinforce that permissions are deliberate, reviewable, and scoped to a real integration use case.

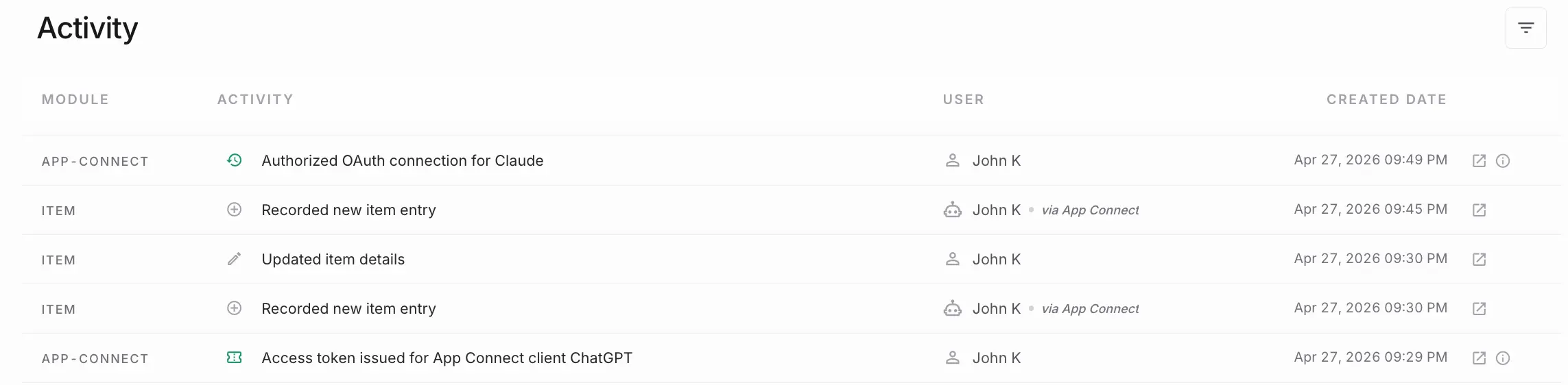

Scope Design Affects Auditability Too

Permissions are not only about prevention. They also affect explainability later.

If an app performs a sensitive action, a finance team may need to know:

- what it was allowed to do

- what it actually did

- which tenant granted the access

- whether the action stayed inside the expected scope

That is one reason scope design and audit history should reinforce each other.

Activity visibility matters because permissions are easier to trust when teams can see how connected systems actually use them over time.

Common Scope Design Mistakes

Teams often weaken their platform unnecessarily when they:

- expose one broad scope for very different financial capabilities

- treat read access to reports as equivalent to write access on accounting workflows

- skip tenant-aware permission reasoning

- grant direct posting power too early

- design scopes around internal implementation shortcuts instead of workflow meaning

These mistakes usually show up later as support burden, customer hesitation, or governance work that should have happened earlier.

A Practical Scope Framework

For embedded accounting platforms, a strong starting point often looks like:

- context scopes for reading company, client, vendor, or report information

- workflow scopes for creating or updating draft operational records

- finance-sensitive scopes for actions that change accounting state more directly

- admin scopes for configuration or install management

Not every platform will use those exact names, but the separation is useful because it mirrors real trust boundaries.

Where Paprel Fits

Paprel is built for teams that need governed accounting workflows, app connectivity, and permissions that match the operational reality of finance systems.

That includes:

- OAuth-based consent for connected apps

- tenant-aware access boundaries

- structured permissions and access control

- workflow patterns that support reviewable, draft-first actions

- activity visibility that helps operators understand what connected systems did

In embedded accounting, good scopes are not a documentation detail. They are part of the platform contract.

Closing Thought

OAuth helps apps get access safely.

Scopes and permissions decide whether that access is actually trustworthy.

The best embedded accounting platforms do not stop at delegated authorization. They turn authorization into a clear, reviewable workflow boundary.

Read Next In This Series

- For the broader auth model, read API Credentials vs OAuth 2.0: A Practical Guide for SaaS Teams.

- For the tenant boundary behind app installs, read Multi-Tenant Accounting Systems.

- For the traceability side, read Audit Trails for Embedded Accounting Platforms.

Engineering notes from the team building Paprel's ledger core and API — ledger architecture, multi-tenancy, idempotency, and the patterns behind audit-grade accounting. Reflects how the system actually works and is updated as the product evolves.

Build in sandbox, launch with a production trial

Use sandbox for developer testing with no billing. When you are ready for real workflows, start production on a monthly plan with a 14-day free trial.